What I'm thinking for Silver.

The $50 support/demand area has yet to be revisited and is a great psychological level as well.

I will still be DCAing either way.

$XAG https://t.co/cjJLAJdC0M

7.1K @CryptoHotep

7.1K @CryptoHotep What I'm thinking for Silver.

The $50 support/demand area has yet to be revisited and is a great psychological level as well.

I will still be DCAing either way.

$XAG https://t.co/cjJLAJdC0M

1

1

0

0

348

348

2 @Munehisa001

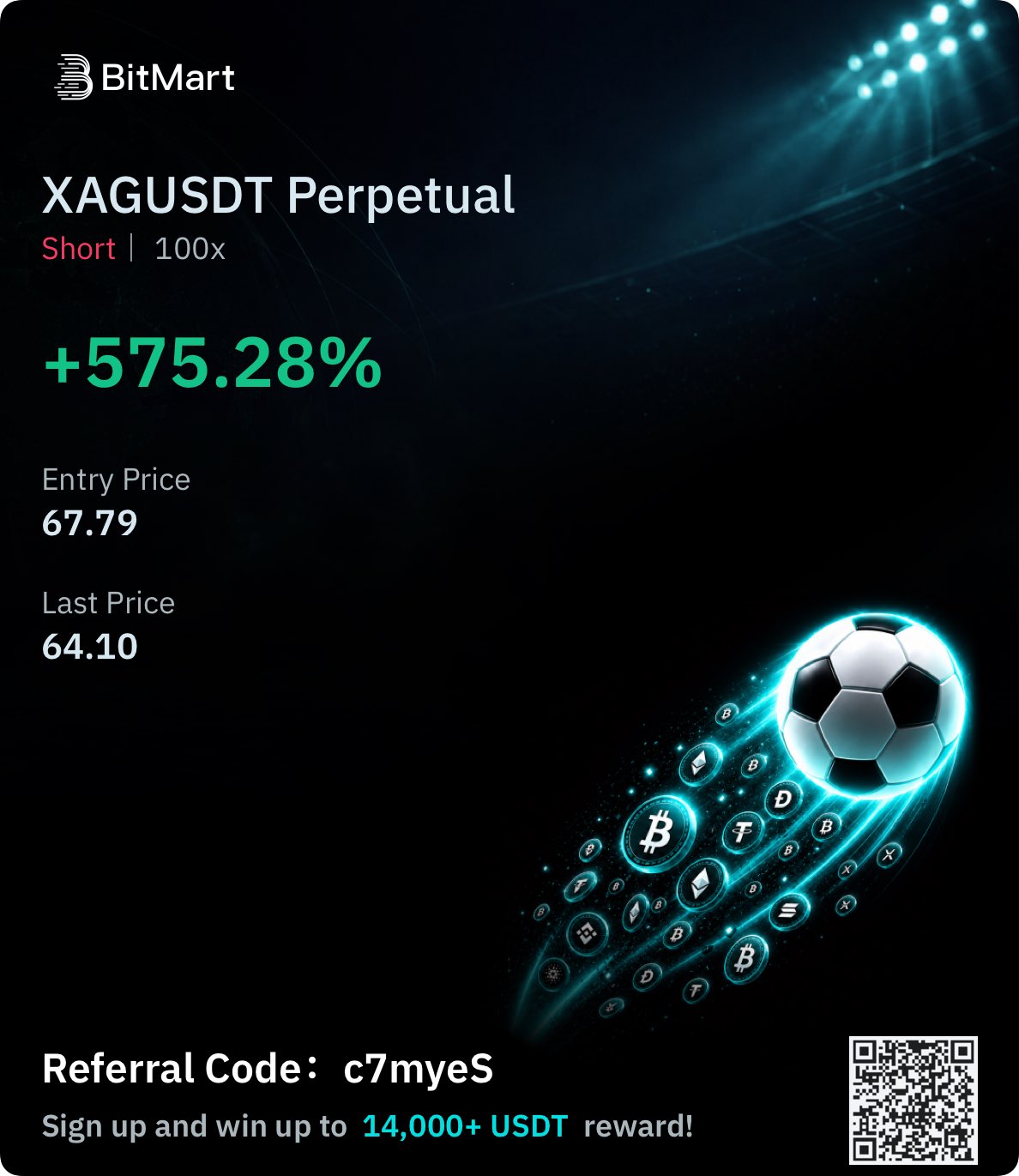

2 @Munehisa001 XAGUSDT https://t.co/LHhhnYMMtV

0

0

5

0

0

5

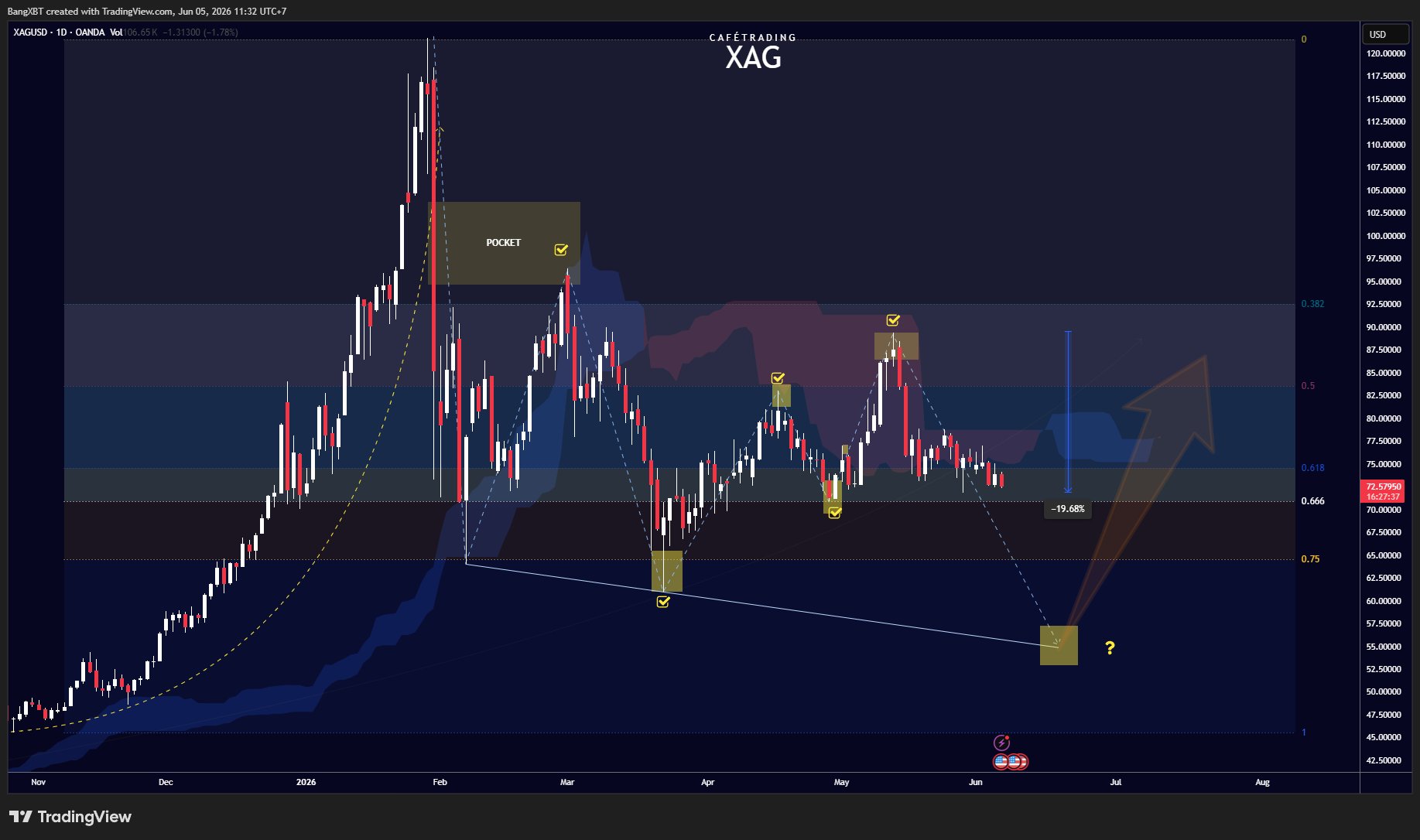

6.4K @BangXBT

6.4K @BangXBT $XAG $SILVER

Come My Way

- MTP -

16

1

2.7K

16

1

2.7K