ether.fi (ETHFI)

ether.fi (ETHFI)

- 67ソーシャル・センチメント・インデックス(SSI)- (24h)

- #30マーケット・パルス・ランキング(MPR)0

- 524時間ソーシャルメンション- (24h)

- 100%24時間のKOL強気比率3人のアクティブなKOL

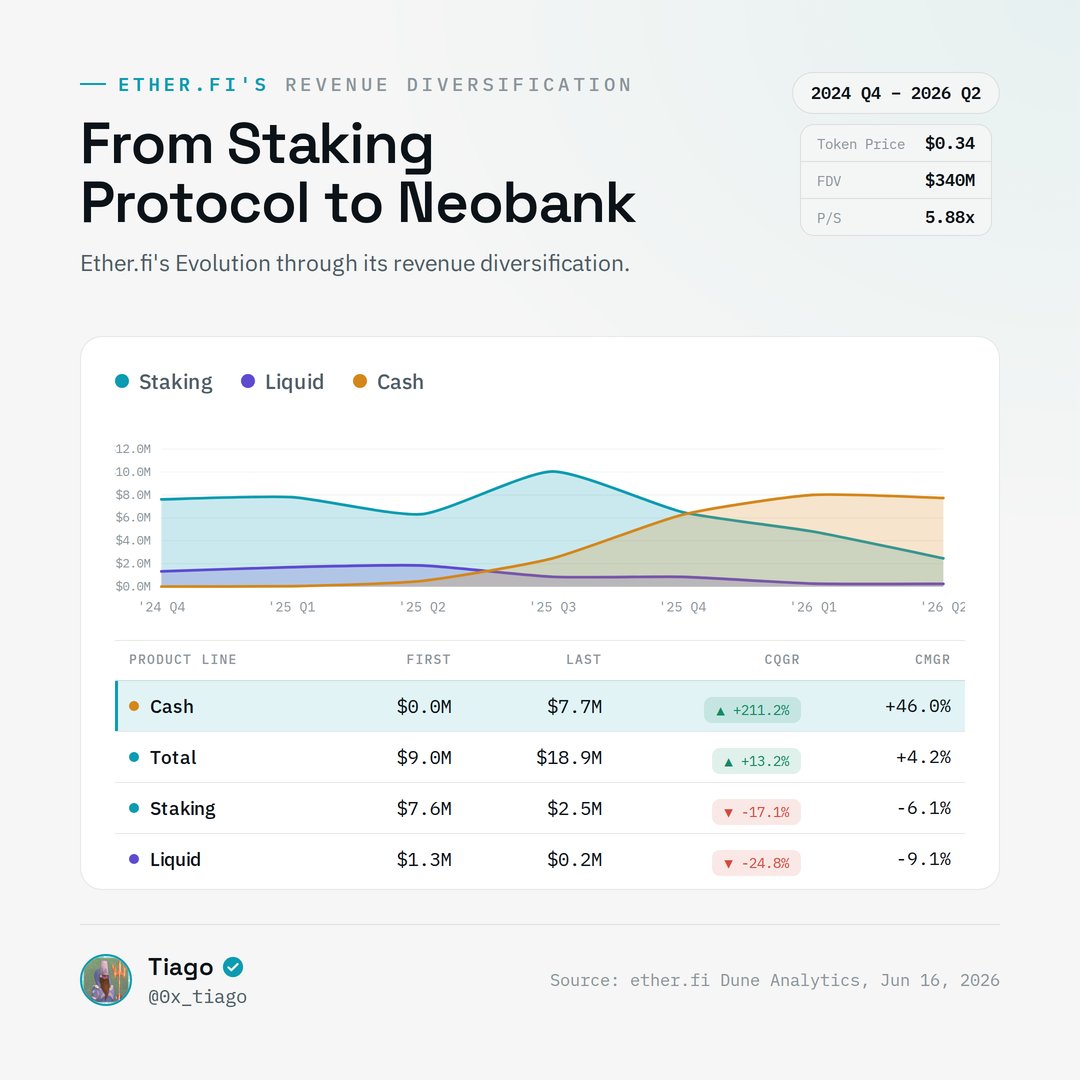

- 概要ETHFI rose 7.99% to 0.3637, finding support at 0.34‑0.35; revenue doubled, cash at 7.7M; however, staking revenue sharply fell, and a KOL says it is undervalued.

- 強気のシグナル

- Price up 7.9%

- Found support at 0.34-0.35

- Revenue rose from 9M to 18.9M

- Cash revenue reached 7.7M

- KOL says it is undervalued

- 弱気のシグナル

- Staking revenue fell to 2.5M

- Still considered a staking protocol

- Social hype remains flat

- Previous downtrend continues

- Potential profit taking

ソーシャル・センチメント・インデックス(SSI)

- データ全体67SSI

- SSIトレンド(7日間)価格(7日間)センチメントの分布非常に強気 (60%)強気 (40%)SSIインサイトETHFI's social hot index remains unchanged at a moderately high level (67.5/100), activity at a full score 40/40, sentiment improved to 25/30 positive, KOL attention low at 2.5/30, driven by a 7.9% price increase and revenue doubling.

マーケット・パルス・ランキング(MPR)

- アラートインサイトETHFI warning rank #30, social anomaly score extremely high at 100/100, sentiment polarization at 50.95/100, KOL attention shift only 2.5/100, mainly triggered by a sudden price surge and revenue spike.

Xへの投稿

Tiago Trader DeFi_Expert B9.72K @0x_tiagoTiago Trader DeFi_Expert B9.72K @0x_tiago

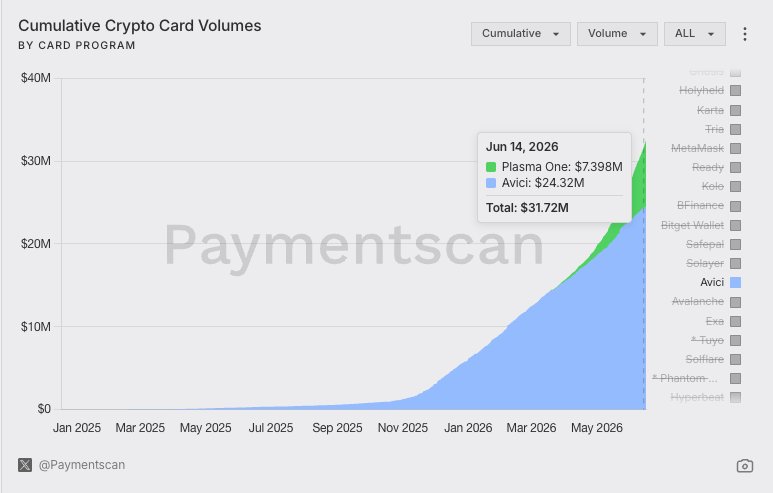

Tiago Trader DeFi_Expert B9.72K @0x_tiagoTiago Trader DeFi_Expert B9.72K @0x_tiagoThe main reason Etherfi is being overlooked by projects such as Plasma and Avici is positioning. Both projects have a lot of loud advocates, while the only loud advocate I've seen for Etherfi is DCF God Avici and Plasma One's combined cumulative volume spent is nearly half of Etherfi's volume in June alone. $ETHFi is one of those opportunities you don't see that often IMO

7 0 635 オリジナル >非常に強気ETHFi交易量远超Plasma和Avici,被认为是难得的被低估的投资机会。

7 0 635 オリジナル >非常に強気ETHFi交易量远超Plasma和Avici,被认为是难得的被低估的投资机会。 EMK TA_Analyst Trader B6.69K @emkfinans

EMK TA_Analyst Trader B6.69K @emkfinans#ETHFI after months of a downtrend is seen forming a low at the main support zone of $0.34‑$0.35. This zone is critically important as it previously saw strong reactions. Targets to watch are $0.55, followed by $0.75 and $1.10. https://t.co/IXmuK18Gtt

39 3 709 オリジナル >リリース後のETHFIのトレンド強気ETHFI is bottoming at the critical support level of $0.34‑$0.35, with targets at $0.55, $0.75 and $1.10.

39 3 709 オリジナル >リリース後のETHFIのトレンド強気ETHFI is bottoming at the critical support level of $0.34‑$0.35, with targets at $0.55, $0.75 and $1.10.- Tiago Trader DeFi_Expert B9.72K @0x_tiago

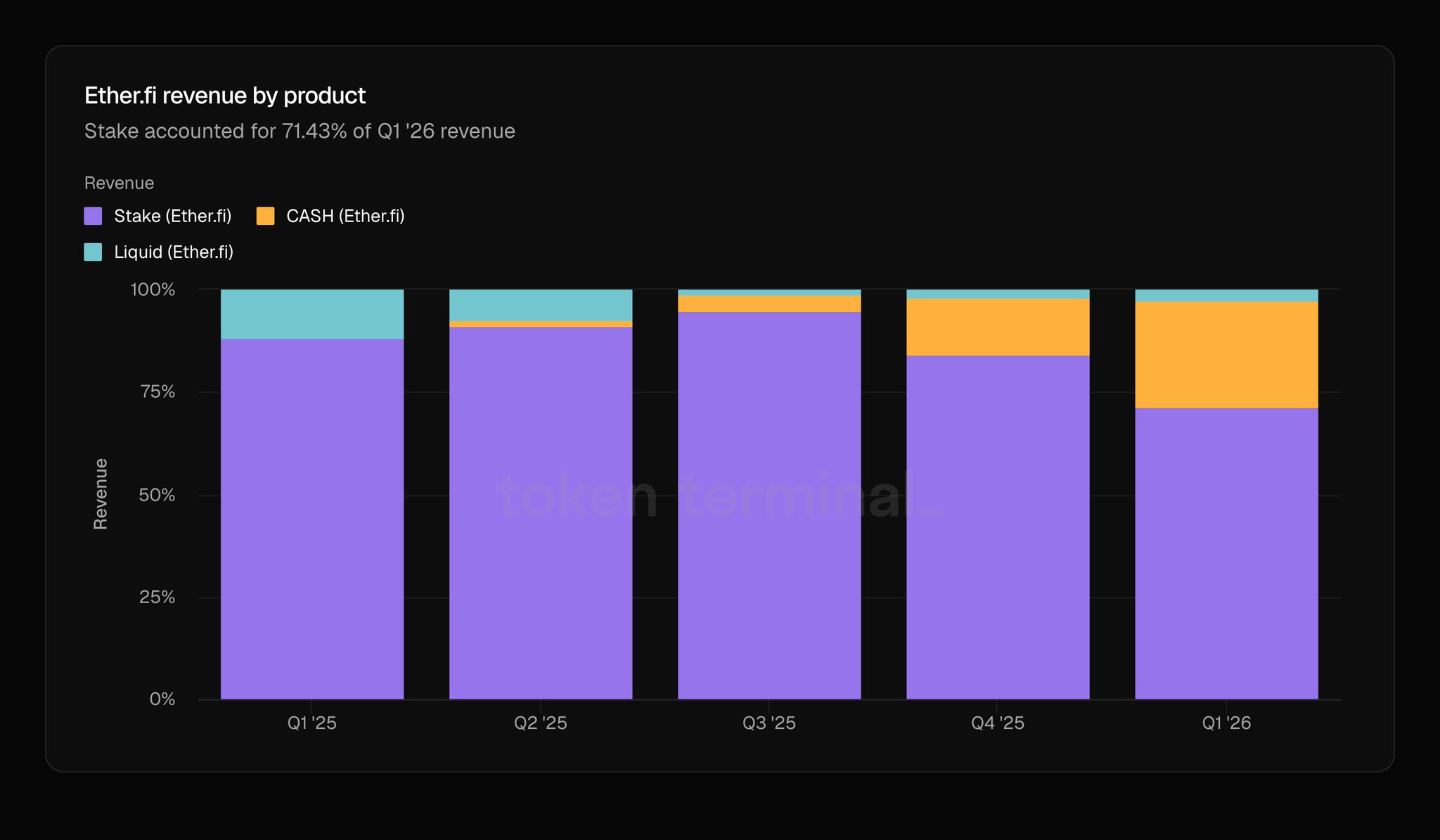

Staking → Asset Management → Neobanking The evolution of $ETHFI’s business in 7 quarters Cash revenue grew from $0 to $7.7M Total revenue grew from $9M to $18.9M Meanwhile, staking revenue declined from $7.6M to $2.5M The market is still pricing it as a staking protocol… https://t.co/MKDIi8Mb5C

2 0 157 オリジナル >リリース後のETHFIのトレンド強気ETHFI's business has shifted from staking to diversification, with cash revenue growing significantly, and the market still undervalues its worth.

2 0 157 オリジナル >リリース後のETHFIのトレンド強気ETHFI's business has shifted from staking to diversification, with cash revenue growing significantly, and the market still undervalues its worth. - Tiago Trader DeFi_Expert B9.72K @0x_tiago

The main reason Etherfi is being overlooked by projects such as Plasma and Avici is positioning. Both projects have a lot of loud advocates, while the only loud advocate I've seen for Etherfi is DCF God Avici and Plasma One's combined cumulative volume spent is nearly half of Etherfi's volume in June alone. $ETHFi is one of those opportunities you don't see that often IMO

7 0 635 オリジナル >非常に強気ETHFi交易量远超Plasma和Avici,被认为是难得的被低估的投资机会。  Ansem TA_Analyst Derivatives_Expert C930.08K @blknoiz06

Ansem TA_Analyst Derivatives_Expert C930.08K @blknoiz06 Sam D10.90K @0xCryptoSam

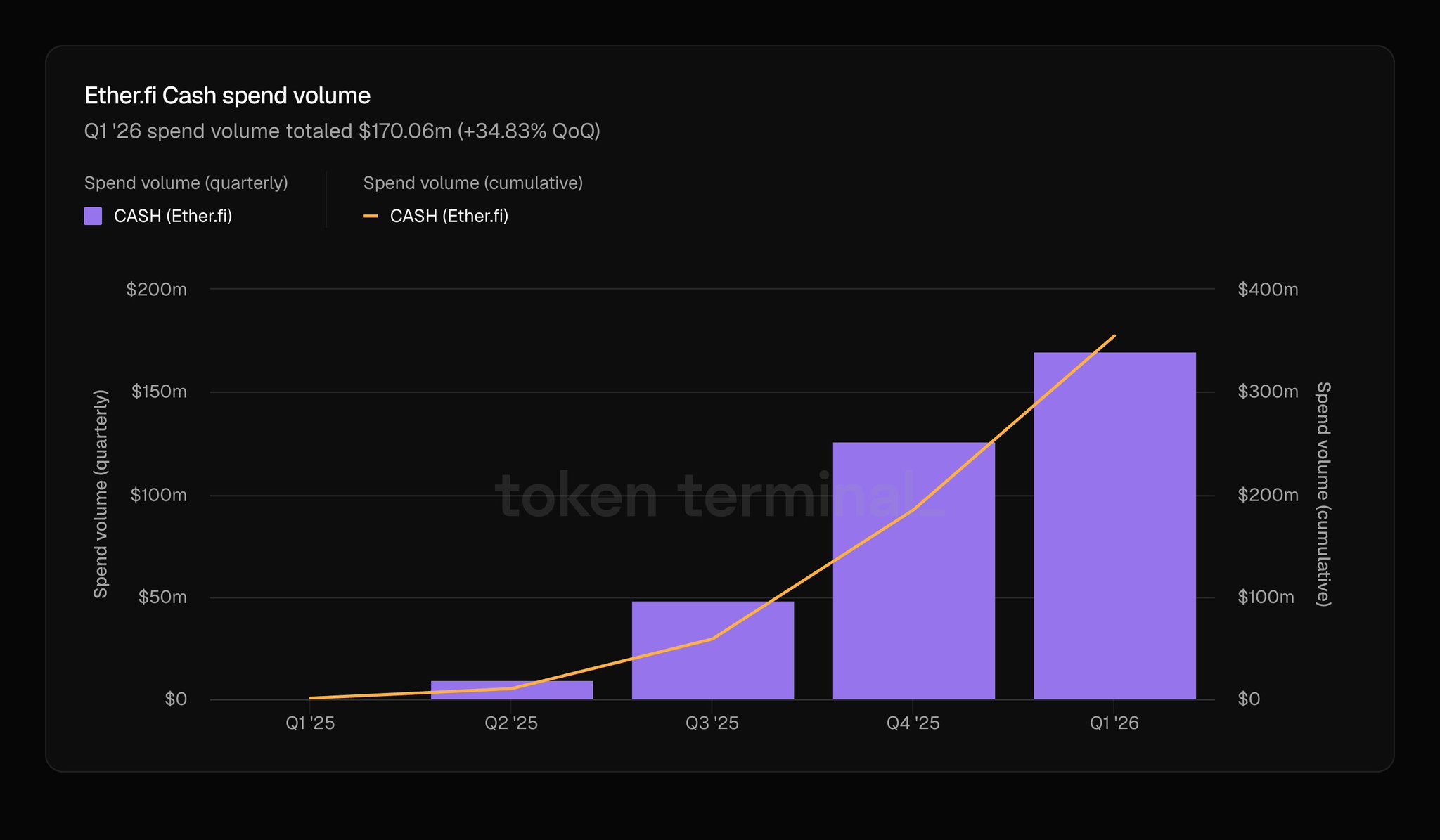

Sam D10.90K @0xCryptoSam@blknoiz06 @MetaDAOProject @AviciMoney ethfi being overlooked for avici / plasma is criminal, they've had great traction and consistent card growth. over $1b annualized spend on their cards. only reason they're undervalued is bc people still think they are an LST business... https://t.co/I4o9CjzqBp https://t.co/Nf6i6eUApc

100 12 25.36K オリジナル >リリース後のETHFIのトレンド非常に強気ETHFI is undervalued by the market despite strong growth in its card business, with annualized spend exceeding $1 billion.

100 12 25.36K オリジナル >リリース後のETHFIのトレンド非常に強気ETHFI is undervalued by the market despite strong growth in its card business, with annualized spend exceeding $1 billion. Emperor Osmo 🐂 🎯 OnChain_Analyst FA_Analyst C92.63K @FlowslikeosmoEmperor Osmo 🐂 🎯 OnChain_Analyst FA_Analyst C92.63K @Flowslikeosmo

Emperor Osmo 🐂 🎯 OnChain_Analyst FA_Analyst C92.63K @FlowslikeosmoEmperor Osmo 🐂 🎯 OnChain_Analyst FA_Analyst C92.63K @FlowslikeosmoI still think the market is not appreciating @EtherFi as a business and continues to value it as a staking protocol. Some thoughts: $ETHFI - fees dropped 26% last month; however, you have to look at their margins to understand the full story. > Gross fees 30d: $12.1M -26.3% > Net earnings: $3.0M/month > Margin: 24.7% > Its now trading at a P/E: 7.57x For comparison, $LDO charges 3.2x the gross fees and has roughly the same net. The difference lies in how revenue is allocated: Lido sent $2.0M to stakers last month, whereas EtherFi's revenue remained in the protocol. - $MORPHO: $0 net on $19.3M gross fees. Trades at $1.26B mcap. - $LDO: 6.0x P/E, 7.9% margin, $2.0M to stakers last month. Trades at $223M mcap. - $ETHFI: 7.57x P/E, 24.7% margin, $0 to holders. Trades at $272M mcap. EtherFi previously returned $3.2M to holders in November. - Nov 2025: $3.2M - Dec 2025: $2.6M - Jan 2026: $1.4M - Feb 2026: $1.35M - Mar 2026: $430K - Apr 2026: $30K - May 2026: $0 - Jun 2026: $0 Consider this a cash hoard

45 15 4.37K オリジナル >リリース後のETHFIのトレンド強気The market undervalues ETHFI as a business, despite its high profit margins and strong user growth.

45 15 4.37K オリジナル >リリース後のETHFIのトレンド強気The market undervalues ETHFI as a business, despite its high profit margins and strong user growth.- Emperor Osmo 🐂 🎯 OnChain_Analyst FA_Analyst C92.63K @Flowslikeosmo

I still think the market is not appreciating @EtherFi as a business and continues to value it as a staking protocol. Some thoughts: $ETHFI - fees dropped 26% last month; however, you have to look at their margins to understand the full story. > Gross fees 30d: $12.1M -26.3% > Net earnings: $3.0M/month > Margin: 24.7% > Its now trading at a P/E: 7.57x For comparison, $LDO charges 3.2x the gross fees and has roughly the same net. The difference lies in how revenue is allocated: Lido sent $2.0M to stakers last month, whereas EtherFi's revenue remained in the protocol. - $MORPHO: $0 net on $19.3M gross fees. Trades at $1.26B mcap. - $LDO: 6.0x P/E, 7.9% margin, $2.0M to stakers last month. Trades at $223M mcap. - $ETHFI: 7.57x P/E, 24.7% margin, $0 to holders. Trades at $272M mcap. EtherFi previously returned $3.2M to holders in November. - Nov 2025: $3.2M - Dec 2025: $2.6M - Jan 2026: $1.4M - Feb 2026: $1.35M - Mar 2026: $430K - Apr 2026: $30K - May 2026: $0 - Jun 2026: $0 Consider this a cash hoard

45 15 4.37K オリジナル >リリース後のETHFIのトレンド非常に強気The market undervalues ETHFI as a business, despite its high profit margins and strong user growth.  YashasEdu FA_Analyst OnChain_Analyst B9.44K @YashasEdu

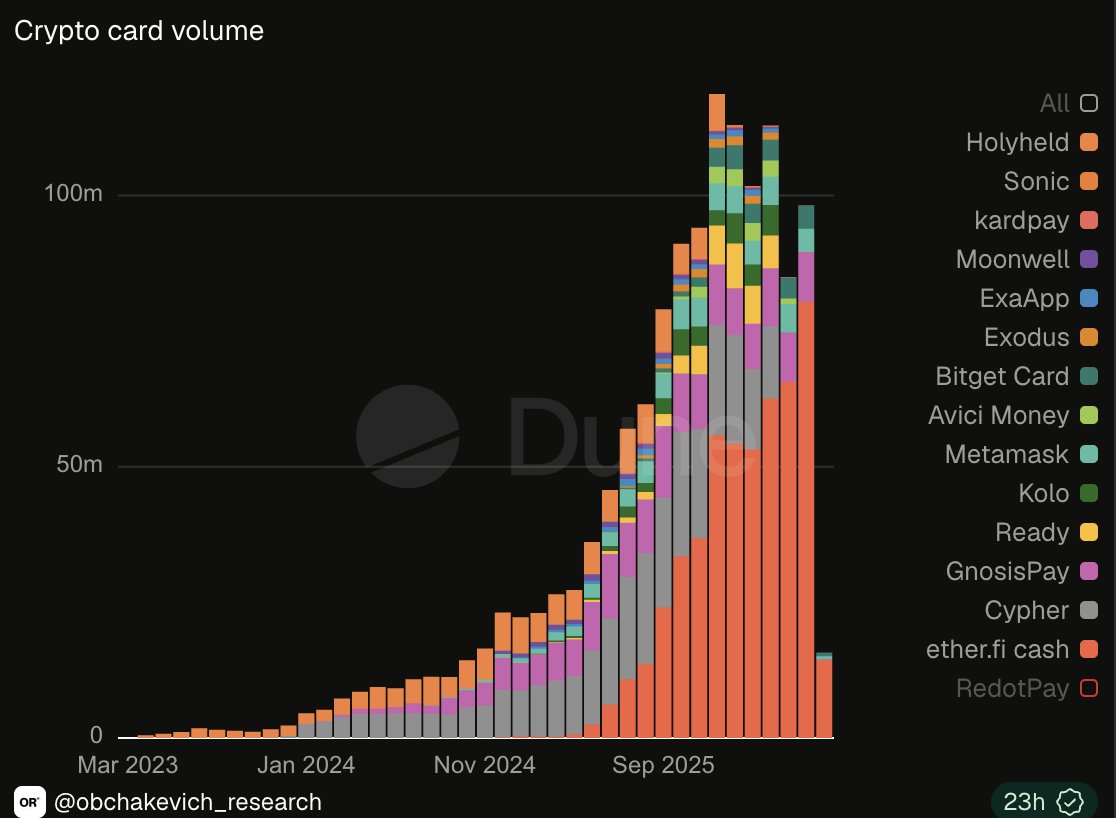

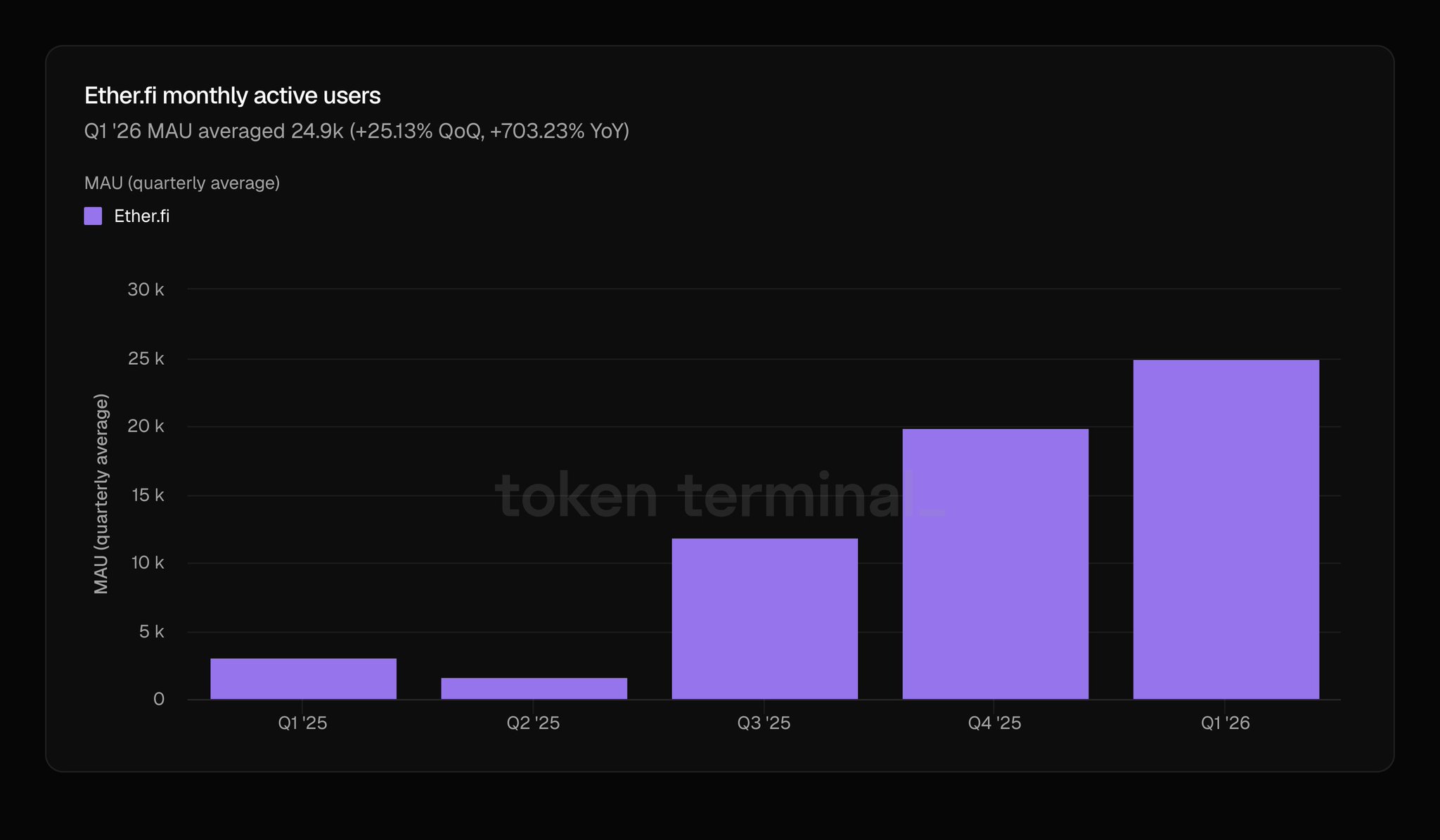

YashasEdu FA_Analyst OnChain_Analyst B9.44K @YashasEduJust noticed that non-custodial card volume is accelerating fastest among sophisticated users taking share through better yields, lower fees and tax alpha. While custodial cards (RedotPay, Cryptodotcom) are winning headcount. Non-custodial (EtherFi, Gnosis Pay, MetaMask) are winning wallet quality. Remember in a regulatory shock scenario, non-custodial cards survive and custodial ones get frozen. h/t to @FourPillarsFP for the data

26 9 1.37K オリジナル >リリース後のETHFIのトレンド非常に強気Non-custodial crypto card transaction volume is rapidly growing, giving it an edge amid regulatory risk.

26 9 1.37K オリジナル >リリース後のETHFIのトレンド非常に強気Non-custodial crypto card transaction volume is rapidly growing, giving it an edge amid regulatory risk. Mars_DeFi Researcher Educator B26.17K @Mars_DeFi

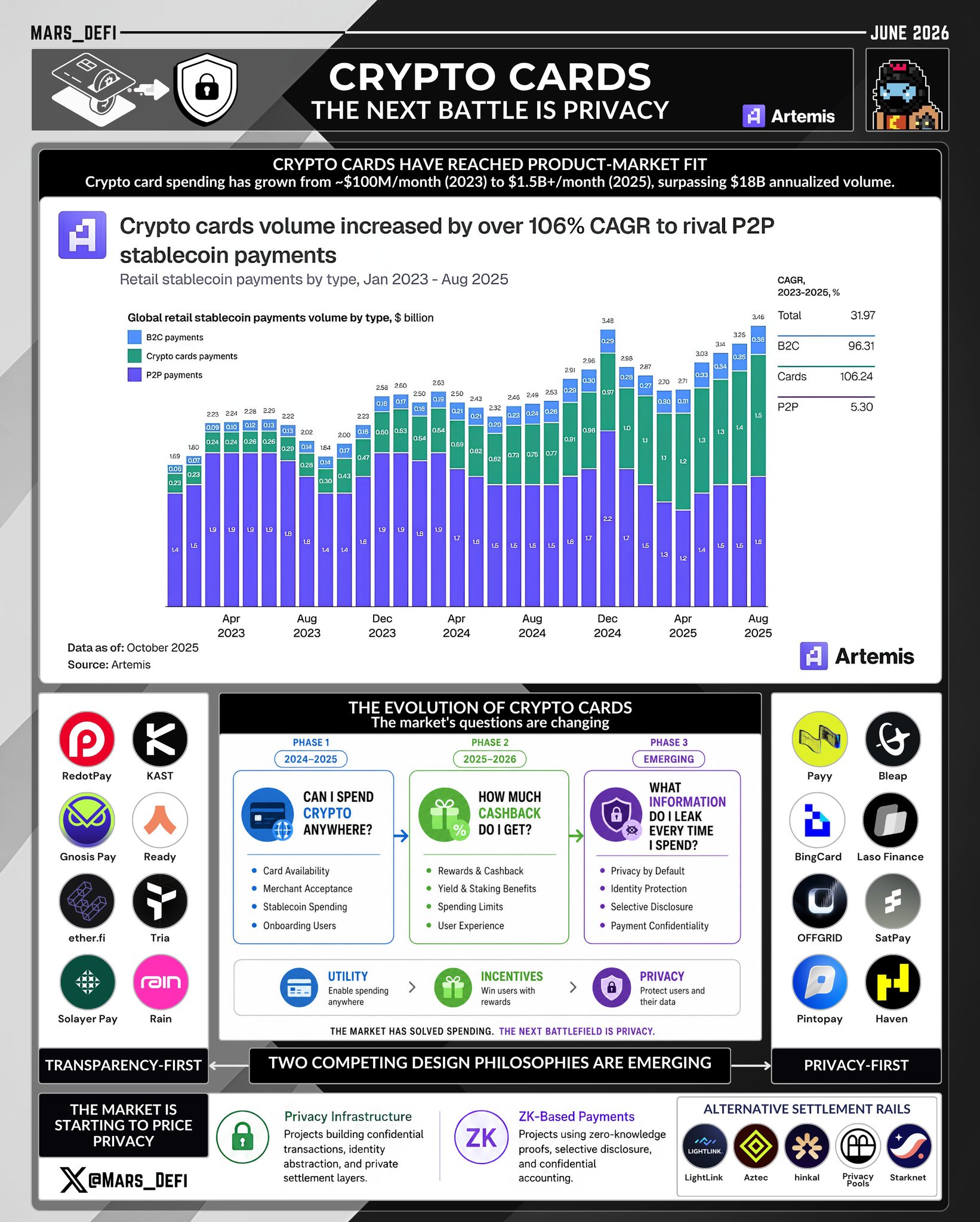

Mars_DeFi Researcher Educator B26.17K @Mars_DeFiCrypto cards have successfully solved spending, but privacy is emerging as the next competitive battleground. For the last two years, the market competed on cashback, yield, UX, and self-custody, but the @ether_fi incident exposed a new challenge: protecting user financial data. Here's what's actually happening: — ● Crypto Cards Have Officially Reached Product-Market Fit Crypto cards have evolved from a niche experiment into a legitimate payment category, with monthly spending volume growing from roughly $100M in early 2023 to more than $1.5B by late 2025. • Cashback rewards • Yield-bearing balances • Higher spending limits • Geographic expansion • Better user experience Over the last two years, competition has centered around making stablecoin payments feel as seamless as traditional fintech and neobank experiences. Today, the category generates more than $18B in annualized spending volume, showing that the industry has largely solved the "Can people spend crypto?" problem. — ● The Conversation Around Crypto Cards Is Changing As the sector matures, users are no longer asking whether they can spend crypto, but what they sacrifice every time they do. • Phase 1 (2024–2025): "Can I spend crypto anywhere?" • Phase 2 (2025–2026): "How much cashback do I get?" • Phase 3 (Emerging): "What information do I leak every time I spend?" This shift reflects a broader realization that what works for DeFi does not necessarily work for consumer payments. — ● The Hidden Tradeoff Behind Self-Custodial Payments Users thought they were getting self-custody and financial freedom, but often received self-custody and radical transparency. The debate is shifting from custodial vs self-custodial to public vs private settlement, and ultimately from wallet ownership to data ownership. — ● Two Competing Design Philosophies Are Emerging As the market shifts toward privacy, crypto payments are beginning to split into transparency-first and privacy-first settlement models. • Transparency-First Most existing card infrastructure is built around public ledgers, where transactions remain auditable, verifiable, and visible on-chain. This model is represented by @RedotPay, @KASTxyz, @ether_fi, @useTria, @gnosispay, @ready_co, @Solayer_Pay, @raincards, and other cards built on public settlement rails. • Privacy-First A newer category is emerging around private-by-default payments and selective disclosure. Projects exploring this direction include @payy_link, @BleapApp, @cryptoBingCard, @LasoFinance, @offgridcash, @sat_pay, @pintopay_me, and @Haven_Hn_. — ● The Market Is Starting To Price Privacy If this trend continues, capital may increasingly flow toward privacy infrastructure, ZK payments, and alternative settlement rails. • Privacy Infrastructure: Projects building confidential transactions, identity abstraction, and private settlement layers. • ZK-Based Payments: Projects using zero-knowledge proofs, selective disclosure, and confidential accounting. • Alternative Settlement Rails: @LightLinkChain, @aztecnetwork, @hinkal_protocol, @0xprivacypools, and @Starknet privacy initiatives. AI has dramatically reduced the cost of wallet clustering, identity discovery, and behavioral analysis, accelerating this shift. — Today, crypto cards compete on rewards, yield, availability, and fees; tomorrow, they may compete on privacy and identity protection. Users are beginning to evaluate not just what they earn, but what they reveal. Crypto payments have largely solved accessibility and rewards; the next battleground is infrastructure that combines self-custody, compliance, and privacy.

Mars_DeFi Researcher Educator B26.17K @Mars_DeFi

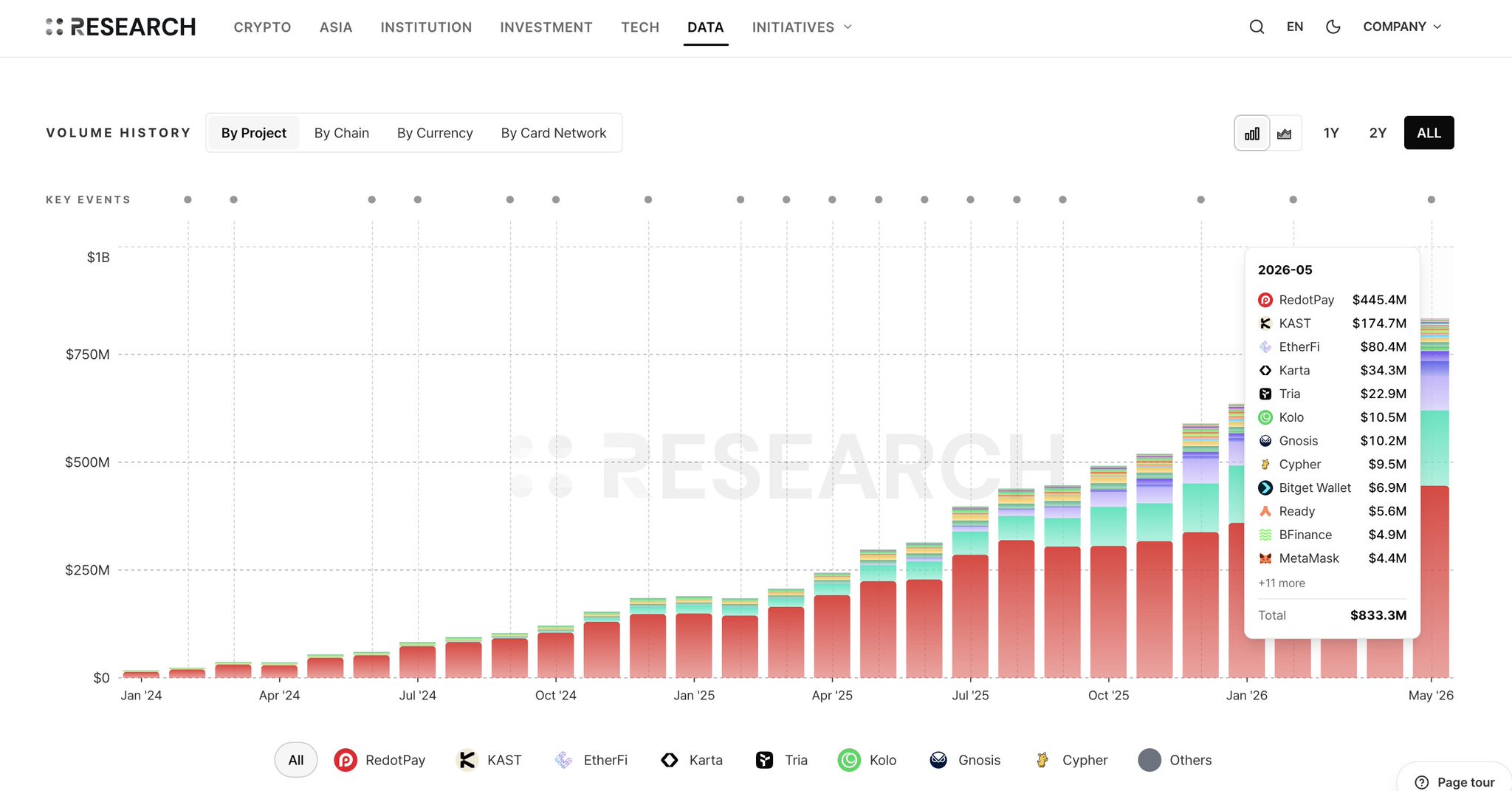

Mars_DeFi Researcher Educator B26.17K @Mars_DeFiCrypto cards have processed over $7.8B in onchain volume, emerging as one of crypto's largest consumer sectors. But beneath the surface, the market is splitting into distinct categories, each competing to become the default financial layer for crypto users. So, which crypto card category is positioned to capture the biggest opportunity? — ● Crypto Cards Are Becoming Crypto's First Consumer Vertical Most discussions focus on cashback, but the real competition is happening across payments, banking, credit, and onchain finance. Over $7.8B in volume has been processed, with most activity occurring in the last 12 months. The top five players account for ~87% of total volume: • @RedotPay • @KASTxyz • @ether_fi • @useTria • @gnosispay Crypto cards have moved beyond experimentation into a category processing billions in real activity. — ● Two Markets Are Emerging Inside Crypto Cards Most CT treats crypto cards as one category, but the data shows two very different markets emerging. • Market #1: Crypto Off

94 47 7.21K オリジナル >リリース後のETHFIのトレンド強気Crypto cards have achieved product-market fit, with privacy emerging as the next key competitive focus.

94 47 7.21K オリジナル >リリース後のETHFIのトレンド強気Crypto cards have achieved product-market fit, with privacy emerging as the next key competitive focus. DeFi Dad ⟠ defidad.eth Educator DeFi_Expert C180.53K @DeFi_Dad

DeFi Dad ⟠ defidad.eth Educator DeFi_Expert C180.53K @DeFi_Dad Marc Zeller D107.59K @Marczeller

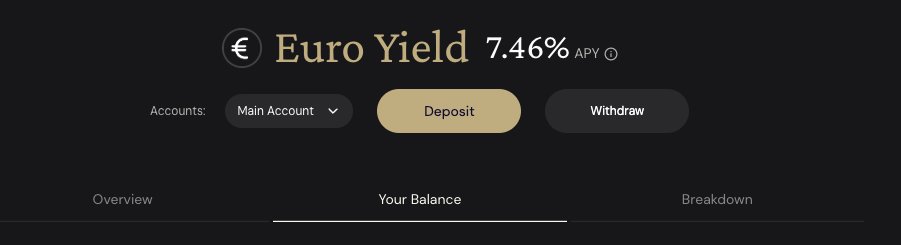

Marc Zeller D107.59K @MarczellerAfter what happened to GnosisPay, I will keep using them, but @ether_fi Cash seems a perfect second card for me as backup. 1) EUR Vault earning 7.4% 2) Borrow and Pay at 4% fixed rate, my collateral earn > than the debt, and a different tax category for me if I borrow instead of "sell stablecoins" to pay 3) higher payment limits 4) bunch of benefits, such as right now 15% cashback on AI spent Disclosure: I'm an Etherfi investor and holder, ref link if u want to try: https://t.co/QVtVCGTKcy

223 28 32.95K オリジナル >リリース後のETHFIのトレンド非常に強気Ether.fi Cash offers 7.4% EUR yield, low borrowing rates and high cashback, the author strongly recommends it.

223 28 32.95K オリジナル >リリース後のETHFIのトレンド非常に強気Ether.fi Cash offers 7.4% EUR yield, low borrowing rates and high cashback, the author strongly recommends it.