In the stablecoin arena, most projects are still grappling with “how to anchor more stability and better liquidity”. However, as more capital moves from TradFi to the chain, mere “stability” is no longer sufficient. What people truly need is a token that retains the dollar’s attributes, continuously generates yield on‑chain, and also incorporates the logic of traditional assets such as gold and US equities.

Recently I noticed that Unitas has become completely different from before. Its earliest core products were USDu / sUSDu – a yield‑bearing stablecoin system that uses a delta‑neutral strategy to make dollar assets earn returns. Simply put, it turns a stable value into an asset that can “work” for itself rather than just lying idle earning interest. At the time, this was a relatively pragmatic entry point: it does not rely on banks or T‑bill narratives, but can capture funding rates and strategy profits as an active asset.

What really merits attention is its recent systematic upgrade from a single product to a multi‑asset layer.

Unitas’s product matrix now spans three directions:

1) Dollar layer: USDu / sUSDu remains the foundation;

2) Gold layer: the new XGLD, backed 1:1 by XAUT (Tether Gold), enables native minting and redemption on BNB Chain, making “interest‑bearing gold” a reality;

3) Equity layer: progressing an Equity Basis Trade, using a delta‑neutral operation of Binance US spot + perpetual contracts to capture the funding rate of the equity perpetual market.

In my view, the latter two steps matter because traditional gold on‑chain has long been “zero‑yield”. XGLD allows it to earn yield alongside dollars for the first time, and the native funding‑rate logic is also applied to equity assets.

These three “legs” essentially diversify sources of return. Previously the model relied on funding rates; now gold and perpetual US equities are added, markedly diluting risk exposure. Notably, the new strategies adopt a “small‑scale validation position + gradual scaling” approach rather than heavy initial allocation, which is a restrained tactic given the current environment.

More crucially, the choice of chain—Unitas has placed its main battlefield on BNB Chain. This is not arbitrary. BSC offers mature spot and perpetual liquidity, natural synergy with the Binance ecosystem (including the recent USDT0 partnership), and relatively friendly RWA soil. They are advancing a strategic partnership with a Hong Kong‑listed company https://t.co/vl6WwvpLC4, with a clear goal: to become the leading yield‑earning layer for RWA assets on BSC.

In essence, this elevates the “yield‑bearing asset layer” concept from a simple stablecoin narrative to a foundational infrastructure that spans dollars, gold, equities and other real‑world assets. Users no longer need to hop between different protocols to achieve yield on various assets within a single framework.

Ultracoin (USDU)

Ultracoin USDU Histórico de Preços USD

Adquira USDU agora

Compre e venda USDU de forma fácil e segura na BitMart.

Ganhar

Coloque suas criptomoedas ociosas para trabalhar e ganhe renda passiva com poupança, staking e muito mais.

Ultracoin X Insight

141.7K @qinbafrank

141.7K @qinbafrank  26

26

39

39

40.6K

40.6K

81.4K @lianyanshe

81.4K @lianyanshe Many people still think of Unitas @UnitasLabs as just having created a stablecoin.

I recently reviewed their product lineup and recent activities and realized this perception is far off; the project has become a yield‑generating asset layer on the BNB Chain, continuously earning cash flow. The protocol already supports multiple assets and yields, and has recently added XGLD (gold yield strategy) and a stock funding rate strategy. For the BNB Chain, this provides stable-yield strategies even in a bear market, boosting TVL and continuously encouraging on‑chain participation. Binance Wallet has consistently offered a 10% annual return, which is actually supported by a variety of strategies.

What is the difference between a stablecoin and a yield‑generating asset layer?

The core of a stablecoin project is anchoring and liquidity; it earns the issuance spread and has little relation to users. The logic of a yield‑generating asset layer is different—it aims to make on‑chain assets productive and generate sustainable cash‑flow returns.

Unitas’s current core products are USDu and sUSDu. USDu is a USD asset layer backed by collateral assets and a portfolio of yield strategies. sUSDu is the interest‑bearing version of USDu, with returns coming directly from the strategies behind USDu.

In most stablecoin projects, the earnings from reserve assets go to the issuer and are unrelated to holders. Unitas’s approach passes strategy yields to sUSDu holders. The protocol’s core capability lies in continuously seeking, evaluating, and integrating new yield sources; as long as a new source passes risk controls, it can be added to the strategy portfolio.

Recently, Unitas introduced a new move on the strategy side: an equity basis trade, i.e., stock perpetual funding‑rate arbitrage, a profit‑making strategy that is only effective in the crypto‑stock market. Many existing yield strategies still rely on perpetual funding rates, but crypto cycles have eroded those returns; the current yields are sustained because of the added stock perpetual funding rate component.

The strategy logic is simple: hold a spot exposure to a stock asset while shorting the corresponding stock perpetual contract. The two positions hedge directional price movements, capturing the funding‑rate return from the perpetual market, similar to standard funding‑rate arbitrage.

Why is this strategy worth attention?

Because crypto funding rates are cyclical; when market leverage demand falls, returns shrink or even turn negative. Stock perpetual funding rates come from users’ demand for tokenized US‑stock exposure, which is not cyclical.

In a weakening crypto cycle, the stock perpetual strategy can supplement yields and reduce sUSDu’s reliance on a single source. No other BSC project appears to be pursuing this path. Unitas’s initial allocation is modest, ranging from $3–5 M, keeping overall risk manageable; the scale can be increased once the strategy stabilizes.

From USDu to XGLD yield‑gold, and now extending revenue sources to stock perpetual contract funding‑rate arbitrage, a multi‑asset, multi‑strategy yield layer is Unitas’s true positioning. Users continue to hold interest‑bearing sUSDu while the underlying strategies evolve with market conditions, eliminating the need to constantly shift stablecoin yields.

31

29

2.2K

31

29

2.2K

71.8K @0xTodd

71.8K @0xTodd Researched the Unitas project, which is basically the BNB Chain version of Ethena.

Launched last year, now the TVL is about 60M, ranking among the top 20 BNB Chain DeFi projects.

First, the Ethena model is familiar to everyone, no need to elaborate; essentially they are investment funds, with fund shares existing in the form of stablecoins.

@UnitasLabs's stablecoin is $USDU, currently with an APR around 10%.

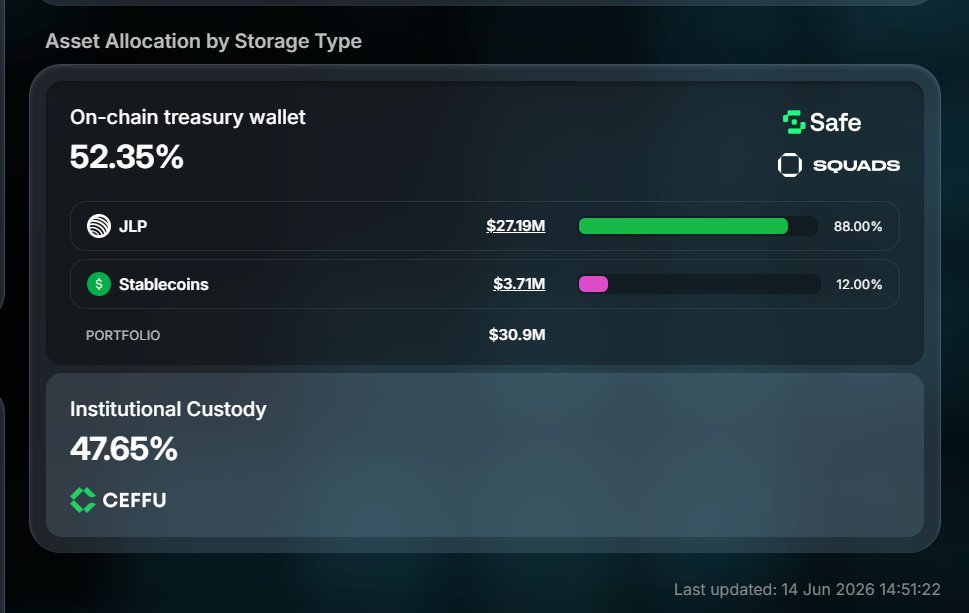

The focus is on the underlying strategy. Unitas is actually cross‑chain on BSC and Solana; the stablecoin is more on BSC, while half of the underlying strategy is in Solana's JLP and the other half is in CEX.

This also brings multi‑chain yield to BSC.

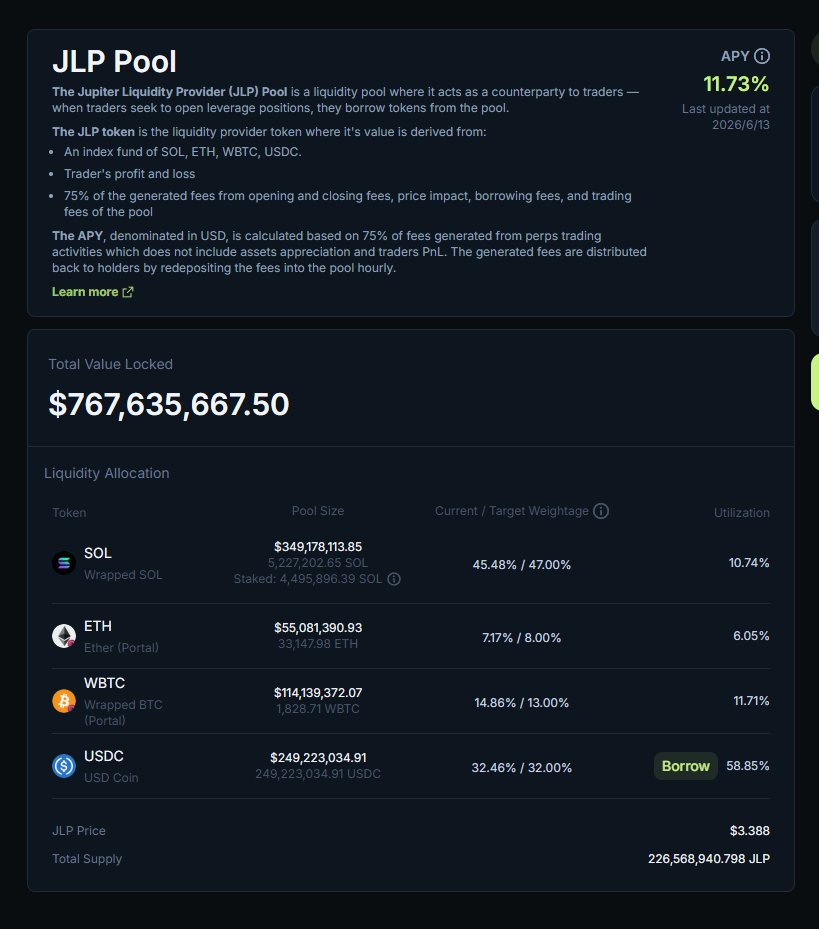

JLP is the opponent liquidity pool for Jupiter perpetual contracts, mainly earning fees plus the losing side of contracts, currently with an APR around 12%.

In theory JLP cannot be perfectly hedged, but engineering can achieve approximate hedging to withstand extreme market blows.

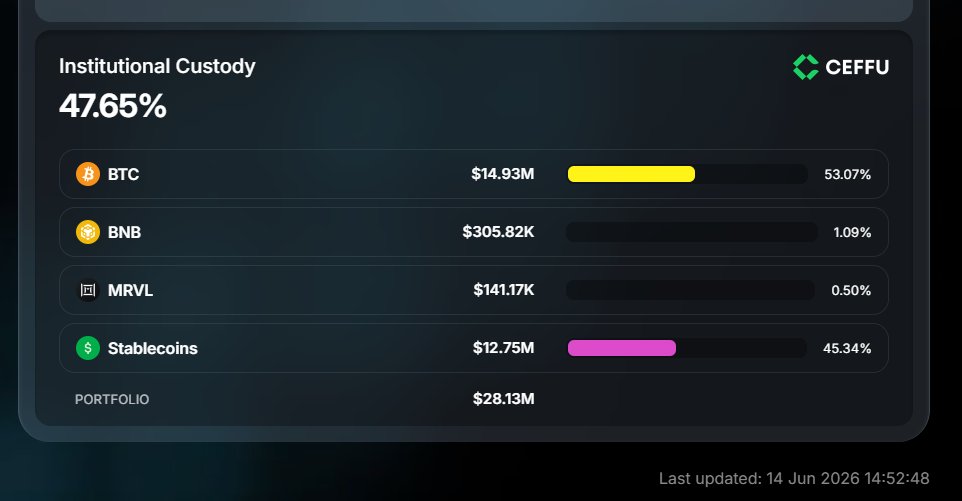

The CEX portion is still custodial in Ceffu. According to Unitas's transparency panel disclosure, the CEX holdings are roughly half BTC and half U positions.

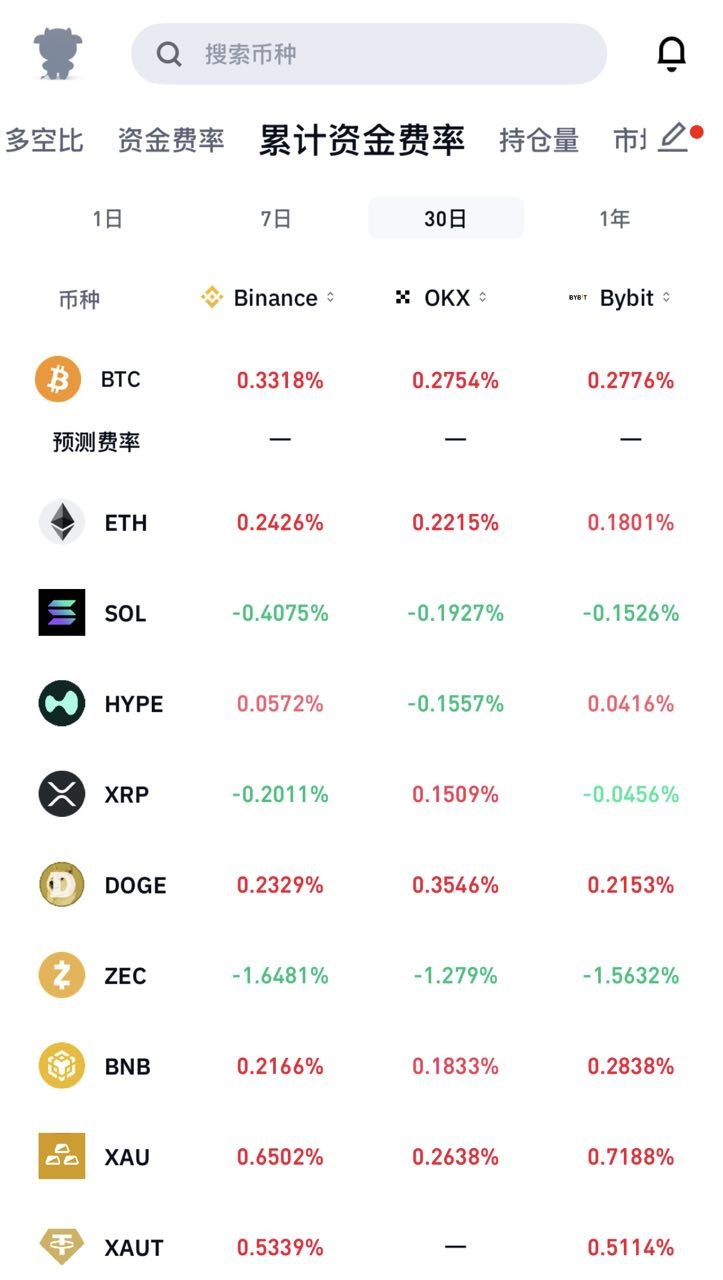

The BTC portion appears to be familiar BTC spot used as margin plus earning the fee on an equal‑size short order; referencing Binance data, the last 30 days is roughly 4%.

The U portion is not clear yet, possibly an intra‑venue arbitrage strategy based on U.

The previous disclosure said that since Binance added US stocks, they can also conduct arbitrage strategies targeting US stocks, still using a long + equal short approach to earn short fees while keeping Delta neutral.

The asset Portfolio is relatively clean and clear.

Regarding USDU itself, currently minting and redemption are limited to a whitelist. If users participate, it is mainly via the secondary market swapping directly with USDT/USDC.

It also looks like they are exploring new directions; besides the U‑based USDU, there is also the gold‑based XGLD.

We also dug into XGLD’s mechanism. Its underlying asset is Tether’s XAUT, pegged 1:1 to gold price; it was recently launched, and there is not much APR data yet.

According to @0xLoki_Zeng, the strategy behind it should roughly be using XAUT as collateral, borrowing U, then running a U‑based strategy.

In fact, swapping XAUT for BTC or ETH can run similar strategies; the principle is the same. However, this product offers extra interest for long‑term gold holders, which is good.

Finally, note that holding USDU alone yields no interest; you still need to stake it to become sUSDU. XGLD does not require this; it carries interest automatically.

17

9

4.2K

17

9

4.2K

Previsão de preço

Quando é um bom momento para comprar USDU? Devo comprar ou vender USDU agora?

Previsão do Beacon

Previsão Probabilística de Preço (Próximas 24 horas)Esta previsão é um produto técnico experimental, fornecida apenas para fins de referência. Ela não constitui uma orientação de investimento. Eventos inesperados no mundo real podem afetar significativamente o comportamento do mercado. Os traders devem tomar decisões com cautela.

Explore Mais

BM Discovery

Nova Listagem