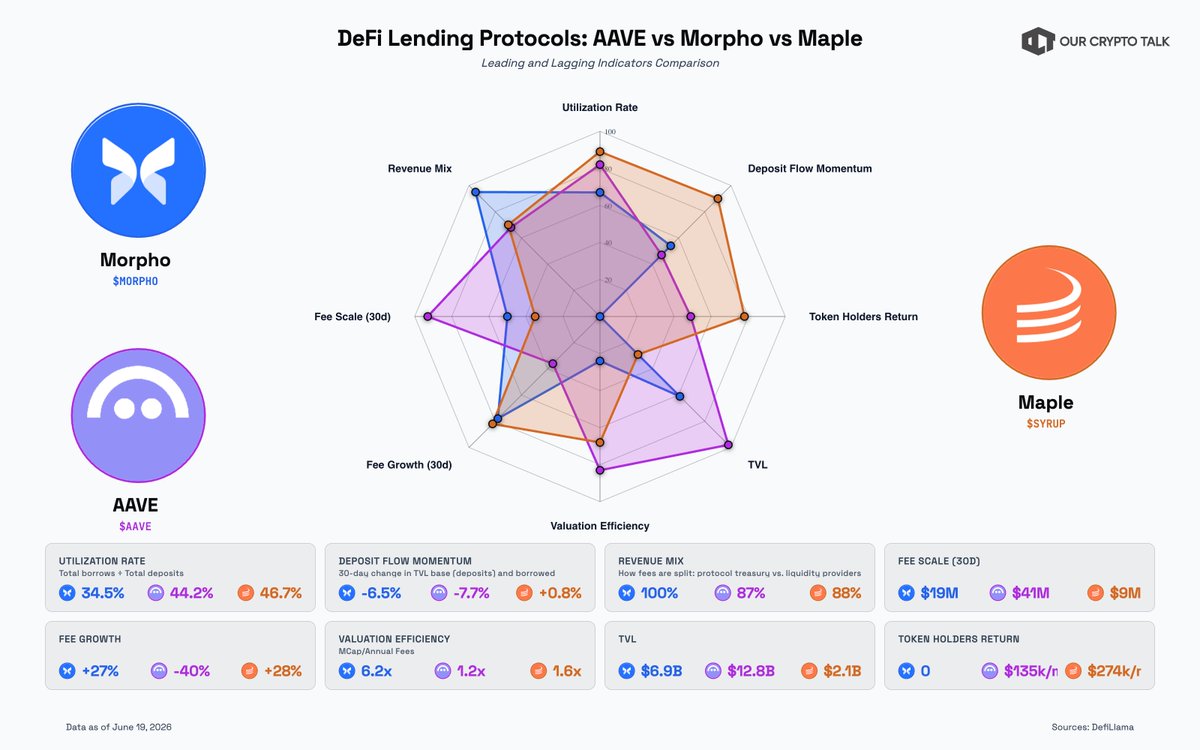

$MORPHO has shown tremendous growth this year, climbing to $7B in TVL.

But what's interesting is that $AAVE and $SYRUP are quietly leading the segment across several metrics.

Let's compare $AAVE vs $MORPHO vs $SYRUP on everything that counts, leading and lagging indicators.👇

➨ LEADING INDICATORS (what moves before the price does)

1⃣Utilization Rate (how hard each deposit base actually works)

SYRUP: 46.7%

AAVE: 44.2%

MORPHO: 34.5%

Maple runs the tightest book in the category. Nearly half its deposits are actively lent out. Morpho's lower number is structural, its curator-driven markets don't deploy all liquidity at once.

2⃣Net Deposit Flows (30d)

SYRUP: +0.8%

MORPHO: −6.5%

AAVE: −7.7%

Maple is the only one of the three taking in capital right now. Aave and Morpho are contracting in near-lockstep, which reads as market-wide deleveraging, not a problem with either protocol.

3⃣ Revenue Mix (who actually gets the fees)

AAVE: 87% to LPs, 13% to protocol

SYRUP: 88% to LPs, 12% to protocol

MORPHO: 100% to