Custody Is the Quiet Gate Every Institutional Settlement Network Has to Clear First

Most analysis of onchain settlement counts banks. The more useful thing to count is custodians, because a regulated institution cannot settle an asset it cannot first hold under its own compliance rules.

This is the step that gets skipped in the excitement about tokenized deposits and tokenized funds. Settlement and custody are not the same problem. A bank can be convinced the rails are fast and final and still be unable to touch them, because its mandate requires qualified custody with specific controls over keys, segregation, and audit. No custody path means no participation, regardless of how good the settlement layer is.

That is why the BitGo institutional custody and wallet integration with Prividium matters more than its size suggests. It is not one more logo. It removes the precondition that blocks every incoming institution before settlement is even on the table.

Consider the order of operations a regulated entity actually follows:

• It must custody the asset within a framework its regulator already accepts.

• Only then can it settle, because settlement moves assets that have to be held somewhere compliant at rest.

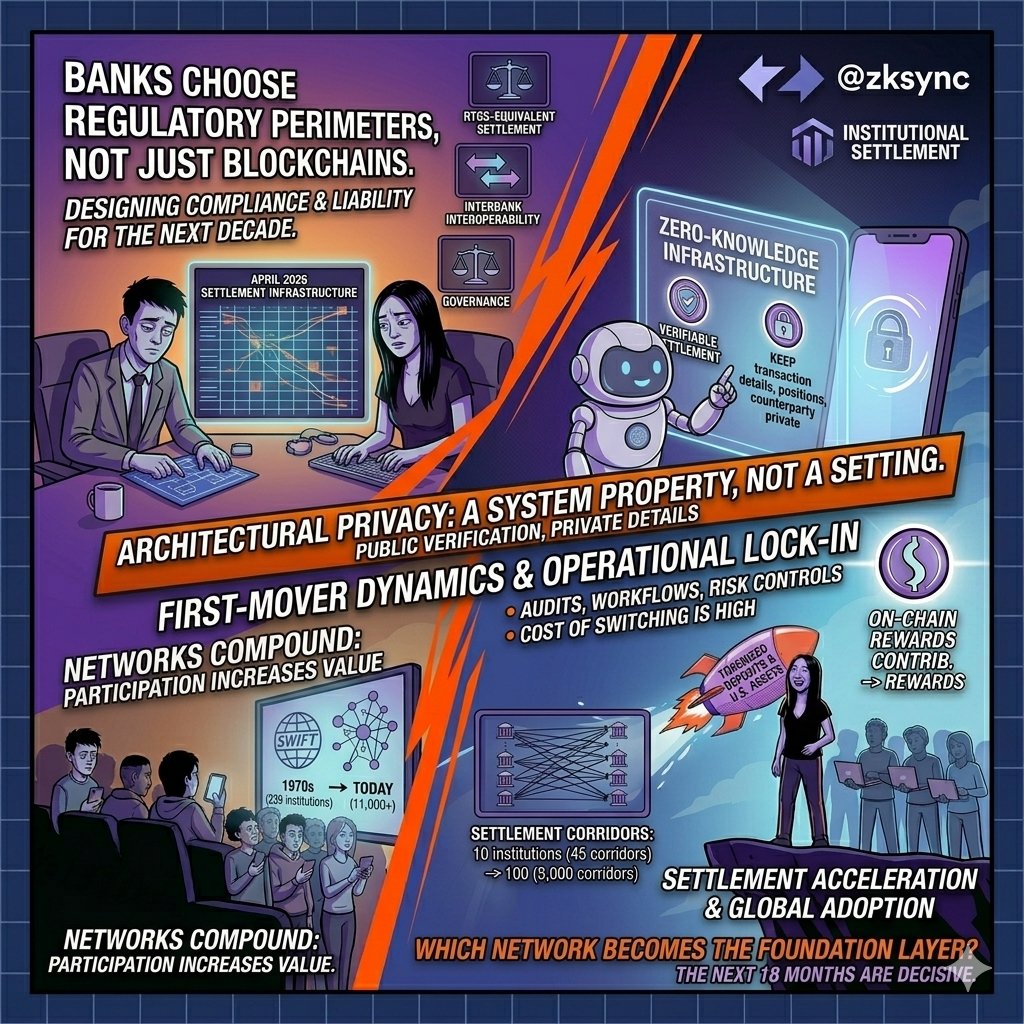

• Only then do network effects apply, because a corridor needs two institutions that can both hold and move.

Seen this way, the deployments on @zksync rails are not parallel announcements. They are a sequence. Custody integration is the part that converts a settlement layer from a demo into something an incoming bank can actually onboard to, because the holding problem was solved before the bank arrived.

The architecture underneath is what makes this hold together rather than a set of separate vendor relationships. Banks execute inside private environments where only zero-knowledge proofs and state commitments reach Ethereum, settlement is final without optimistic challenge windows, and the same stack carries custody, execution, and interop instead of stitching them across teams.

Here is the part worth contesting: the institutional race in 2026 will not be decided by whoever has the fastest proofs or the most famous bank logo. It will be decided by whoever made it boring and compliant to hold the asset in the first place, because that is the step that quietly gates all the others.

For anyone who has actually sat through an institutional custody and settlement review, which gate really decides whether a bank can join a network: the speed of settlement, or the holdability of the asset at rest?