Comprar cripto

tarjeta

Comercio P2P

Compra USDT en un marketplace

Tarjeta de crédito/débito

Compre criptomonedas con Visa o MasterCard

Pago vía prestadores

Compre criptomonedas a través de MoonPay, Simplex y más

Tarjeta BitMart

Impulsando su experiencia con las criptomonedas

Tarjeta prepago de criptomonedas

Obtenga una Mastercard lista para usar al instante

Comerciar

USDⓈ-M

Utilizando USDⓈ como colateral

COIN-M

Utilizando la propia moneda como colateral

TradFi

Trading integral para metales, acciones y forex

Operativa de demostración

Aprenda a operar con riesgo cero

Resumen de futuros

Plataforma única para todo lo relacionado con futuros

Rey de Futuros

Pool de premios de 478 000 USDT

Crecer

Resumen de Earn

Activos inactivos, gane con facilidad

Ahorros

Gane intereses conservando su portafolio.

Staking

Staking sencillo, cuantiosas retribuciones.

Gestión de patrimonio

Aumente su riqueza con un equipo de activos top

RWA

Mantenga BMRUSD, disfrute del rendimiento

Exclusivo VIP

Gane de forma estable para usuarios VIP

Rewards

Centro de recompensas

Descubra recompensas exclusivas por valor de hasta 14 000 USDT

LaunchPrime

Una plataforma para lanzar tokens y NFT

Programa de afiliados

Únase para ganar cuantiosas comisiones

Powerdrop

¡La solución AirDrop de próxima generación ya está AQUÍ!

Centro de eventos

El centro unificado para todas las operaciones de trading

Sorteo diario de futuros

100 % de probabilidades de ganar con operaciones diarias

Sorteo diario de Spot

Gane 8888 USDT en grandes premios

Recarga móvil

Recargue móviles de forma fácil, online y segura

Send

Send money globally, fast and secure

BitMart Mall

Viva de las criptomonedas

MetaMask USD (mUSD)

$ 0.99 (mUSD/USD)

0.00%

24H

MetaMask USD Datos de precios en tiempo real

El precio de hoy de MetaMask USD es de $ 0.99 (mUSD/USD). Con una capitalización de mercado de $ 35.67M USD. Volumen de trading en 24 horas de $ 35.59M USD, Un cambio de precio en 24 horas de +0.00%. Y un suministro circulante de 35.71M mUSD.

MetaMask USD mUSD Historial de precios USD

Siga el precio de MetaMask USD para hoy, 7 días, 30 días y 90 días

Periodo

Cambiar

Cambio (%)

Hoy

$ 0

0.00%

7días

$ 0

0.00%

30días

$ 0.0099

-0.99%

90días

$ 0

0.00%

Sea propietario de mUSD ahora

Compra y vende mUSD fácil y seguro en BitMart.

MetaMask USD Información de mercado

$ 0.99 Autonomía de 24 horas $ 0.99

Máximo histórico

$ 1.10

El mínimo histórico

$ 0.74

Cambio en 24 h

0.00%

Volumen en 24 h

$ 35,594,102.15

Suministros en circulación

35.70M

mUSD

Market Cap

$ 35.67M

Suministro máximo

--

Capitalización de mercado totalmente diluida

$ 35.67M

Trade mUSD

Ganar

Pon a trabajar tus criptomonedas inactivas y obtén ingresos pasivos a través de ahorros, staking y más.

MetaMask USD X Insight

MichaelK.eth

Security_Expert

Educator

B

29.1K @mikashi

29.1K @mikashi Alcista

Paying for coffee with MetaMask and the mUSD stablecoin, showcasing the convenience of everyday cryptocurrency use.

doodlifts D

15.2K @doodlifts Afternoon coffee by @MetaMask paid for directly in $mUSD stablecoins

My keys, my coins, my coffee https://t.co/Q6CiBhNWyM

68

68

9

9

1.9K

1.9K

2026-05-27 23:37

Tendencia de mUSD tras el lanzamiento

Alcista

Paying for coffee with MetaMask and the mUSD stablecoin, showcasing the convenience of everyday cryptocurrency use.

🐺 FREKI ANCIENT CRYPTO OG 2011 | HBAR XRP BTC FLR

Influencer

Media

B

10.8K @Freki_OG Alcista

Santiment最新开发排名显示MetaMask mUSD、Hedera和Chainlink等项目活跃度领先。

Hedera is a phoenix. D

1.2K @SYCR6h8A4qUyAHf https://t.co/yZua8LhIOX

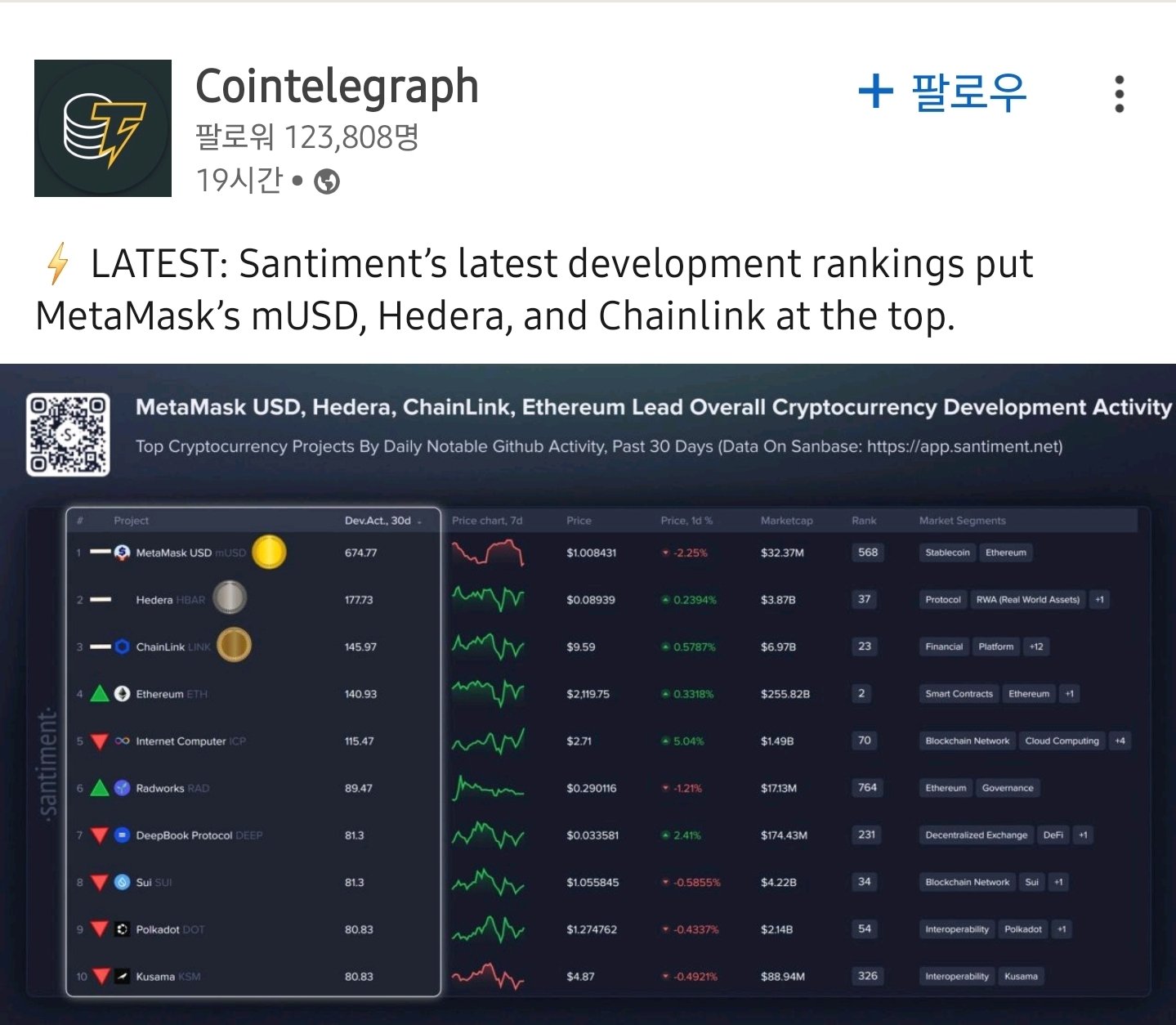

#Cointelegraph

LATEST: Santiment's latest development rankings put MetaMask's mUSD, #Hedera, and Chainlink at the top. https://t.co/zjexFrSC4M

24

1

325

24

1

325

2026-05-26 15:57

Tendencia de mUSD tras el lanzamiento

Alcista

Santiment最新开发排名显示MetaMask mUSD、Hedera和Chainlink等项目活跃度领先。

Cointelegraph

Media

Influencer

D

2.9M @Cointelegraph Neutral

Santiment's latest development rankings show that mUSD, Hedera, and Chainlink are at the top.

⚡️ LATEST: Santiment’s latest development rankings put MetaMask’s mUSD, Hedera, and Chainlink at the top. https://t.co/A7cKOXuFI9

95

40

15.1K

95

40

15.1K

2026-05-25 20:11

Tendencia de mUSD tras el lanzamiento

Neutral

Santiment's latest development rankings show that mUSD, Hedera, and Chainlink are at the top.

Predicción de precios

¿Cuándo es un buen momento para comprar mUSD? ¿Debería comprar o vender mUSD ahora?

Al decidir si es un buen momento para comprar o vender MetaMask USD (mUSD), es importante ajustarse primero a su propia estrategia de trading y perfil de riesgo. Los inversores a largo plazo y los traders a corto plazo suelen interpretar las condiciones del mercado de forma diferente, por lo que su decisión debe reflejar su enfoque personal. Según el último análisis técnico de 4 horas de mUSD, la señal de trading actual es Comprar. Según el último análisis técnico de 1 día de mUSD, la señal actual es Comprar.

Predicción de Beacon

Pronóstico probabilístico de precios (próximas 24 horas)Descargo de responsabilidad de la predicción de Beacon

Los resultados de los datos que se muestran en esta página se analizan en función de los datos de trading reales (OHLCV) del par de trading seleccionado junto con los indicadores técnicos correspondientes.

Esta predicción es un producto técnico experimental y se proporciona solo con fines de referencia. No constituye un consejo de inversión. Los acontecimientos inesperados del mundo real pueden influir significativamente en el comportamiento del mercado. Por tanto, los traders deben tomar decisiones con precaución.

Esta predicción es un producto técnico experimental y se proporciona solo con fines de referencia. No constituye un consejo de inversión. Los acontecimientos inesperados del mundo real pueden influir significativamente en el comportamiento del mercado. Por tanto, los traders deben tomar decisiones con precaución.

Sobre MetaMask USD

MetaMask USD (mUSD) is a cryptocurrency and operates on the Ethereum platform. MetaMask USD has a current supply of 35,709,327.585263. The last known price of MetaMask USD is 0.99974642 USD and is down -0.02 over the last 24 hours. It is currently trading on 18 active market(s) with $4,363,064.20 traded over the last 24 hours. More information can be found at https://metamask.io/price/metamask-usd.

Leer más

Enlaces oficiales

Explorador de blockchain

Explorar más

BM Discovery

Nuevo listado

RE Re Protocol

-- 0.00%

O o1.exchange

-- 0.00%

METAKPK Botchain

-- 0.00%

CTM C8ntinuum

-- 0.00%

SPCXON SpaceX Tokenized Stock Ondo

-- 0.00%

ATEG ATEG.DV

-- 0.00%

GCOIN G COIN

-- 0.00%

$BLAST SafeBLAST

-- 0.00%

SPYON SPDR S&P 500 Tokenized ETF (Ondo)

-- 0.00%

QQQON Invesco QQQ Tokenized ETF (Ondo)

-- 0.00%